Out-Competing China Starts With The Tax Code

Two provisions of the 2017 tax cuts are critical to great power competition.

Tariffs are almost always the main issue connecting the tax reform debate with strategic competition with China. However, some provisions of the 2017 Tax Cuts and Jobs Act (TCJA) should get some of that attention, especially the 100 percent bonus depreciation and the research and development (R&D) amortization.

The major individual tax cuts and reforms introduced in the TCJA are scheduled to expire next year. While much of the focus will be on those individual tax cuts, the business provisions will be important for the U.S. economy’s position in the world, particularly relative to China.

China and the United States might appear to have similar corporate taxes. The United States has a federal corporate income tax of 21 percent and, once various state-level corporate income taxes are added, a combined rate of 25.8 percent. That’s just a hair above China’s standard corporate tax rate of 25 percent. However, statutory corporate taxes tell only a small part of the story. While one obvious difference is that China provides many tax exemptions for specific regions and industries, a more subtle difference is at play, too. The tax code’s base (how corporate income is calculated) is crucial for how a corporate income tax affects the economy. Perhaps the most important part of corporate tax base design is how firms deduct investment costs.

The TCJA introduced a policy called the “100 percent bonus depreciation,” which allowed companies to fully deduct the cost of their investment in short-lived assets like equipment and machinery. Without bonus depreciation, companies must spread the deductions for their investment throughout an asset’s life. This creates a tax bias against investment: companies can immediately deduct operating costs but cannot immediately deduct capital investment costs, penalizing new investments that raise worker productivity.

According to recent estimates, the TCJA’s reforms boosted long-run domestic capital investment by 7 percent, with both the lower corporate tax rate and 100 percent bonus depreciation playing key roles. However, 100 percent bonus depreciation started phasing out in 2023. Under current law in 2024, companies are only eligible for 60 percent bonus depreciation, and the policy will fully phase out by 2027. Reintroducing 100 percent bonus depreciation permanently would re-incentivize investment in equipment, particularly key labor-saving equipment like industrial robots.

TCJA moved in the opposite direction for R&D investment because of five-year R&D amortization. The policy was intended as a budget gimmick to reduce the on-paper cost of the TCJA over the course of the budget window. However, Congress never got around to canceling the policy, and it took effect in 2022.

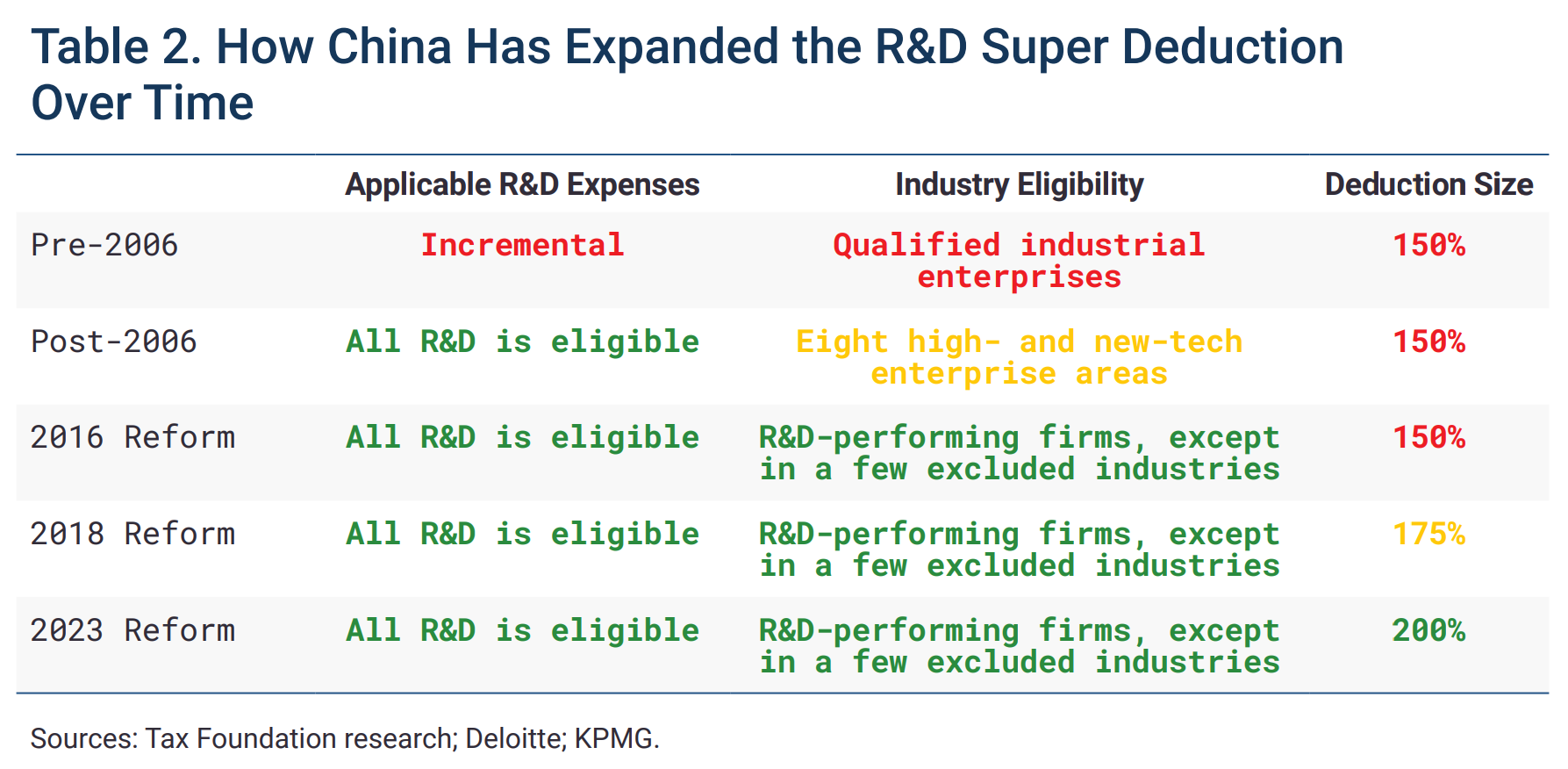

Worsening the tax treatment of R&D in the United States stands in stark contrast to China’s pro-R&D tax policy. A large part of China’s economic strategy to control cutting-edge technology is transitioning from the world’s factory to the world’s R&D lab, and its R&D spending has grown rapidly as a share of GDP in recent years. To aid this goal, China has a super deduction for R&D expenses, which allows companies to deduct over 100 percent of their R&D. The result is a substantial tax subsidy, and they have expanded it in recent years. Starting in 2023, China implemented a 200 percent super deduction. In practice, under a 25 percent corporate tax rate, that translates to a 25 percent government subsidy for R&D investment. Meanwhile, U.S. R&D amortization imposes a tax penalty of around 2.5 percent.

{kind=link}

Reversing R&D amortization and fully reinstating a 100 percent bonus depreciation are economy-wide policies, improving investment incentives no matter the industry. However, they both have a disproportionate impact on specific sectors of the economy. Getting rid of R&D amortization would particularly help manufacturing, given manufacturers are responsible for over half of R&D investment. Capital-intensive industries benefit more from the ability to deduct equipment purchases, given that equipment is a larger share of their overall costs, and semiconductor manufacturing requires more sophisticated equipment than just about any other industry.

The United States also has a historical precedent for improved deductibility of capital investment as a tool for reindustrialization and even rearmament. In 1940, when former General Motors executive William Knudsen arrived in Washington to head up defense production, one of his first steps was allowing companies to take deductions for investment in defense production-related assets faster.

Lastly, it is worth remembering how cheap these policies are in the context of the broader tax debate. Extending bonus depreciation and reintroducing R&D spending would only cost $609 billion over the ten-year budget window, relative to the cumulative cost of $4.2 trillion to extend the whole package. They’re also much cheaper than the major industrial policies recently enacted, with the CHIPS and Science Act and the Inflation Reduction Act cumulatively accounting for roughly $1.2 trillion over a decade.

Punishing China with tariffs has been central to the economic competition narrative. But, to strengthen the U.S. economy, businesses need to reinvest, and that’s where the economic policy conversation should start.

Alex Muresianu is a Senior Policy Analyst at the Tax Foundation, focused on federal tax policy. Follow him on X: @ahardtospell.

Image: Dilok Klaisataporn / Shutterstock.com.